Company Profile: Hikari Tsushin

Part 1: The Berkshire Disciple

Disclaimer: The content on this website is for informational and educational purposes only and is not created to meet your personal financial situation. Nothing should be considered as investment advice or as a guarantee of profit. You are advised to consult with your financial advisors to discuss your investment options and whether it would be a suitable investment for your personal needs. The information used in this publication is from sources that are believed to be reliable but the accuracy cannot be guaranteed. It may include some errors, please make sure to do your due diligence. The opinions expressed are those of the author and the author only. These opinions are subject to change without prior notice.

I’ve been wanting to write this for some time now. It’s a fascinating business and perhaps one of the most unique companies you’ll ever encounter. The company has a long history and a whole lot of drama over its period of existence. This also makes for a fantastic story to tell, and unfortunately, not retold enough in the English-speaking world (nor in Japan quite frankly). It’s also fun to write about because it just has so many faces, and depending on how you frame it, there’s a completely different story to tell. It’s the founder, the culture, the business journey, philosophy and it all has it’s own story to tell.

The bottom line though is that this IMO is a Japanese company with the most capitalist mindset I’ve come across. Theres a very good reason why EPS has compounded at a 16% CAGR over the last 10 years.

They care about IRR, they care about shareholder returns, having a margin of safety and ultimately finding asymmetric opportunities. That is, they want limited downside versus the upside. They are a rare breed in Japan being a company that has both a well defined operating strategy as well as a capital allocation framework. Simply put, they think like investors, first and foremost.

To the extent that in their presentation to individual investors, they even flat out put how much their company should be worth today. ¥2.5trn. Explicitly stating that they are undervalued.

It’s fascinated me because I felt such a disconnect in the way that this company gets perceived in Japan versus how it is by international investors! Historically, the company had a bit of a notorious reputation here, but outside, lauded as the ‘Japanese Berkshire’. This inconsistency in perception by locals, of course, may also mean it’s misunderstood by local market participants - a potential source of alpha.

Based on my personal conversations at least, if I were to summarise how Hikari is seen by foreign investors in one word, it’s probably “Buffett”. If I had asked someone Japanese, it’s probably “Scary”.

So the topic of conversation when Hikari is mentioned is always so different when I speak to international investors vs locals that it fascinates me.

I feel for Graham Rhoades, who wrote a fantastic piece on this company, but got some heat for calling it a Berkshire Hathaway of Japan. I totally understand where he is coming from and actually I think it’s pretty damn close . Also, I thought it was such a great piece of writing, which highlights some details/history of the company and was a great resource, so I urge you to check it out. I understand why it’s compared to Berkshire. For one, Hikari’s largest holding in its public equity book is literally.. Berkshire Hathaway. Until recently, they also had an corporate website in the vibe of Berkshires own website. The company applies many of Berkshire’s core principles in Japan and at a scale many haven’t been able to. As a compromise, I call it the Berkshire Disciple.

It is an interesting business as a potential investment opportunity, but more than that, this is a company that keeps showing up in the stocks I own or like. (ahem… I get in before they do… 66% of the time). In otherwords, they tend to find business that I also personally find remarkable. So I’ve been spending some time trying to understand them as Investors.

Since I’m also not an investor in Hikari and I think the Graham and others has already written a pretty good profile on the stock, rather than it being a typical investment write-up, I thought I’d try to capture the “Japanese Perception” of Hikari and discuss things that may be more focused on the culture of the firm. Call it a collection of interesting stories. I‘ve been getting feedback from other Japanese investors and went through as many Japanese publications, and interviews of former employees to capture interesting stories. So I’ll profile the company’s two faces namely:

Hikari Tsushin, the Operating Business & Hikari Tsushin, the Investor

Whilst both are just as important and the combination of it is why it makes this company so special, just to avoid becoming another 45 minute+ read I’m going to break it up. In part 1 I will be covering the operating business. (It’s still 30 mins tho lol)

Part 1: Hikari Tsushin, the operating business

In this write-up, I’ll be covering:

Business Description

Business model focused on Recurring revenues

Competitive advantage

Growth Opportunity

Management

Hikari’s Unique Culture

How business is perceived by Japanese people - Hikari’s Dark past and how it’s improved today

The Business

Today, the business houses close to 140 subsidiaries and 100 equity method affiliates and close to 700 investments in publically listed companies.

Founded in 1988, Hikari has been around for quite some time, and whilst throughout the years it has continued to evolve and transform, you could argue that this is a well-established business. Hikari Tsushin means Optical Communication Network, which is related to their original business. In classic Buffett’s “Berkshire Hathaway” naming though this is simply an old relic, and today the business goes way beyond that. Depending on how you want to frame it, it’d be quite difficult to describe Hikari Tsushin as a business - in a nutshell though, Hikari Tsushin has been a Sales force driven distribution company. They focused on providing distribution capabilities to a wide array of industries and end markets.

But it’s not just that, Hikari has an investment portfolio consisting of cheap Japanese stocks. Through their investments, they’ve been able to realise an IRR of 17% per annum over the last 7 years - which is extremely impressive if you think about the fact the TOPIX and Nikkei has performed WAY below that. Something like low to mid single digit CAGR. Quite frankly this performance beats many investors. Again, no wonder why this business gets compared to Buffett.

A Brief History

This website provides some really great historical info on Japanese companies including Hikari.

The journey of Hikari’s comeuppance to date, was volatile. The company rose to fame at a metioric pace and just as quickly faced a near death experience. The term roller coaster I think is too mild an expression.

The company emerged during Japan's late 80s economic bubble, a period of rapid growth in technology and telecommunications. It quickly gained traction by capitalizing on the burgeoning demand for mobile phones and office solutions in the 90s. This was the first big wave they rode.

They were distributing office equipment like copiers, fax machines, and telephones. Then it later expanded into telecommunications where they focused on mobile phone sales and subscription services - another fast growing market back then. They managed to ride this mobile phone boom in the 90s, becoming a key distributor for major telecom carriers like NTT Docomo. Their ascent was so fast that by 1996, Hikari Tsushin had gone public, and its valuation soared as it was seen as a darling of Japan’s ‘tech-driven’ economy. At its peak, the height of the dot com bubble in early 2000, the company's market capitalization reached over ¥1trn, and its founder, Shigeta-san, was briefly listed among the world’s richest individuals. Hikari became one of the Japanese poster childs of the dot com bubble.

Bubble Burst and Recovery

Then everything came crumbling down. The dot-com bubble burst in 2000 and hit Hikari Tsushin hard. The company had overextended itself with aggressive expansion and risky investments, particularly in their flourishing mobile phone biz, which unexpectedly turned unprofitable due to fraudulent activity by staff that inflated sales (more on that later). In one fell swoop, they had to revise down their profits into a significant loss. Their stock recorded 20 consecutive days of limit downs. It got so bad it went down from peak to trough by 99.5%!!! Quite something…

This crisis forced a major restructuring. Shigeta-san then invested ¥10bn of his own capital to restructure the company. Since, the company shifted focus toward more stable revenue streams, such as corporate telecommunications services and insurance sales, while reducing its reliance on volatile consumer mobile phone sales i.e. not recurring at all. Arguably though, this was first of many ‘iterations’ that lead to what Hikari Tsushin is today.

By the mid-2000s, Hikari Tsushin had begun to stabilize and it turned profitable again. Their saving grace was their focus on selling Sharp copy machines with a ‘lease’ model. It also expanded its insurance division, targeting small and medium-sized enterprises (SMEs). Looking back, this was likely the moment managment realised the true value of ‘recurring revenues’. It ultimately paid off, as it regained investor confidence and saw steady growth in the latter half of the decade.

The company today (from 2010–Present):

Since 2010, Hikari Tsushin has re-emerged with its position as a diversified holding company with operations across telecommunications, IT services, insurance, energy etc, etc.

Today the business has 7 segments which it split out its revenues by. Even within these segments though, the businesses can be diversified.

A key feature and focus by management though is that while some of the things they sell are capital intensive to produce, the business insists on being asset light. Being able to sell, and selling well is their main goal. Thus their focus is really to find good suppliers who’s product whether as their own or a 3rd party brand they can push. One key change it has seen over the last decade has been their focus on selling their own services and products in a fabless manner, this of course means Hikari can achieve a much higher ROI, something they are uncompromisingly focused on. Still today you can see that their own products continue to increase as a share of their revenue, and quite rapidly.

Their focus on ROI has also meant that they’re increasingly reducing their headcount at what was once a highly people driven sales team. Instead they are now focusing on having partners that can manage sales activities for them.

Recurring everything

When we think about a diversified portfolio of recurring businesses, it’s easy to think of businesses like Constellation Software which does this within software but diversified by vertical. Hikari goes further.

What is truly interesting about Hikari is that today, it doesn’t have so much a sector specialisation per se, but rather a business model specialisation. Namely, the business focuses on what’s called ‘stock type revenues’ in Japan i.e. more globally known as recurring revenue. Since the traumatic dot com bubble experience, the company’s key strategy has been to grow and expand its recurring revenue streams across a variety of industries and and re-invest that into both their operating business + investment portfolio. More than 80% of their revenue is considered recurring today.

This wasn’t always the case of course as we touched in the history of Hikari. But through the ruthless downturn in their business, Hikari has adapted, to become a more resilient business for the future. I believe, with hundreds of subsidiaries, diversified across a multitude of businesses they probably have one of the most unique customer acquisition/retention datasets in Japan and if not the world.

The management today purely focuses on this business model with some strict operating rules around a) how much does it cost to acquire a customer b) how long will they be in contract and c) what the the return on investment would be over time. Whilst I’m not aware of the specific ‘exit criteria’ for them to abandon a business, it sounds like they’ve got pretty specific metrics in mind before pulling the plug. One KPI management insists, is that for Hikari as a group, they want to achieve an IRR above 30% for their operating business.

What Hikari looks for are monthly contracts that can span years aimed at SMEs and Consumers. Naturally in order to do this, Hikari is willing to take a loss in the first year - but in a span of 5 years wants to ensure to achieve an attractive IRR.

And when I say diversified, its diversified. As you saw, it can be anything from energy, internet subcriptions to even a water server subscription business! and as a matter of fact, this business is a listed company called Premium Water Holdings (2588.JP) a company that was acquired by Hikari operating on their core principles.

They have some fun businesses too.

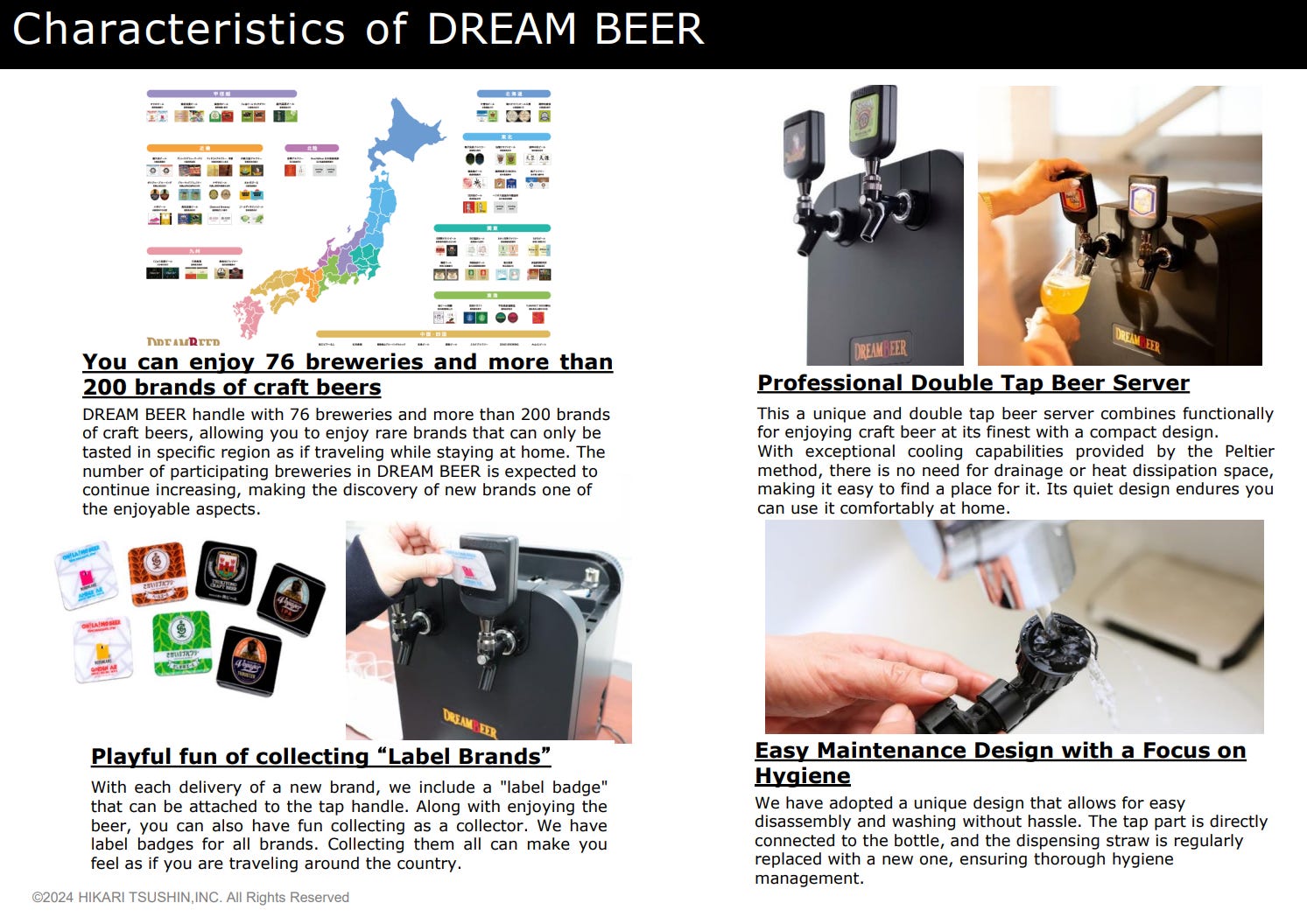

As you can see, as long as you can build a profitable, recurring business model out of it, it doesn’t really matter. Take DreamBeer for example, which they started in 2020. This provides a subscription beer server which can send you a batch of craft beer from regional areas of Japan either bi-weekly or monthly. It’s a pretty neat business as it helps feature close to 200 local craft beer brands and this will likely grow over time. Simply put, this employs the playbook of Premium Water Holdings. Actually, Premium Water themselves are investors in DreamBeer!

Maybe the genius in this industry agnostic ‘business model specialisation’ is that whilst it gets harder to assess the business with much granularity as an investor over time, Hikari will create whats effectively a funnel for a diversified recurring revenue stream. As they keep creating new streams in new industries/markets, Hikari will increasingly have a portfolio of uncorrelated businesses that provide steady cashflow that’s not dependent on a single industry. Though still a large portion still comes from Utilities for instance, this could be something that can truly provide protection from the whims of the economy, something which I’d suspect they are still scarred fom the past.

The fact they structure these businesses through hundreds of subsidiaries may be an advantage too. Practically, Hikari in the past had a pretty ugly reputation in Japan, I think to some extent it still haunts them. However, the use of it’s subsidiary may mean customers may not even realise it is owned by hikari and effectively insulates the parent entity. (BUT this part is just a wild guess..)

Hikari’s Competitive Advantage

So whats the competitive advantage if this is a company selling all kinds of things? I think ultimately it comes down to its distribution network that it has built and consequently the extensive customer base it has established over the years. The company boasts a massive network of 1.3 million corporate customers, 4 million consumers and 1000 sales partners which houses more than 20,000 sales staff. Of this, 1/3 are run by former Hikari Employees. They also have exclusivity agreements with their partners to ensure that they don’t sell competitor products. In any case, this is an incredible army of people that will be selling on Hikari’s behalf.

Whilst I don’t like to use this word too lightly, this therefore means to some extent this business has a a network effect as the business continues to increase the number of suppliers/products available and can sell it to their existing customer base. With some products being so general in it’s use case, I do think there is an opportunity for Hikari to cross-sell other services/products in its portfolio. (For e.g. If a customer has a utility contract, why not try using their internet service too? or beer, hehehe..)

I think their other more intangible moat is the culture they have fostered throughout the decades of trial and error. I will expand on that later on. But their relentless focus on customers and Buffett style return on investment focus can create a powerful environment for shareholder value creation.

Growth Opportunity

Since the business is diversified across multiple industries, it is open to doing anything and everything so long as it can set up a recurring money stream at their IRR hurdle rate. So, at least in theory, the potential total addressable market is extremely large. Whilst the TAM is something that it less easily quantifiable, it’s comforting to know that Hikari has demonstrated a long track record of success across multiple end markets - which suggests the odds of them succeeding in a new market is better than average. Taking this into consideration, the runway can be quite long!

The company currently sees the largest growth potential in energy, insurance and beverage where they already have a relatively large exposure. Within these there seems to be a relatively stable market growth opportunity. In addition to that however, it seems to me that Hikari has some opportunities to gain market share. For example in their electricity business their market share is 2.8% by supplied volume. In their delivered water business it’s 31% and in short term insurance it’s 8.5%. So while end markets are pretty diversified, the formula for growth seems to be quite similar.

Which in my mind is:

Low/mid-single digit market growth + market share gains.

Ultimately the company targets a 10% CAGR on recurring profit growth over the next 10 years.

If I had to guess, they’ve probably set out this target with some margin of safety, and could do better than this. Hikari expects some of this growth to come from M&A - which they have been increasingly vocal to complement it’s organic growth. They see a potential to acquire both publically listed companies as well as private ones and about 30% of their operating profit they claim, has come from M&A so it’s pretty significant. Over time as it becomes harder to scale organically due to the sheer size, they see themselves doing more M&A to sustain the current earnings growth rate. As of now the CEO sees the IRR potentially starting to decline in 5 to 7 years time as a result of it’s size. The focus nonetheless remains the same, which is to maximize the ROI, while limiting the downside risk.

Management

The detail of the founder despite the size of the business he’s managed to build remains a mystery. He’s been meticulous in maintaining his privacy so it’s been hard to find details about his background. So private that not even is direct reports know much about him! His upbringing seems to be quaint. Born in Tokyo, to a father who was a lawyer - and a family that was considered ‘elite’. Despite that he started his own venture which is something almost unthinkable in that time. (I mean, doing ‘start-up’ even a few years ago was still seen as ‘risky’ in Japan).

He was a maverick, he started Hikari at the age of 23 and saw a meteoric rise during the dot-com bubble and eventually he became (back then) the youngest founder to ever list on the Tokyo Stock Exchange, at the age of just 34. Due to this tremendous success, and after the IPO he momentarly ranked as the 5th richest person in the world. Others also recognised his prowess. Hikari became one of the main sales distributor for then flourishing and now well-known SoftBank and its diversified telecom services. Shigeta-san even sat on their board alongside the founder, Son Masayoshi and were both figures that defined the Dot com boom in Japan.

One interview that provided a hint of what kind of CEO he was came from an interview with Mr. Koji Yamamoto, who was one of the top-class salesmen at Hikari and had become a Director at the tender age of 28. He has since started his own company and also has a YouTube channel where he discusses his business and at times, touches upon his past experiences at his former employer. On his YouTube he gets asked by his colleague about the founder of Hikari Tsushin and you can already tell he’s reluctant to talk about him in any capacity from the get-go, and it almost seems like this comes from a place of deep respect and to some extent, a bit of fear. I’ve summarised some of his comments.

In one word, the founder was a philosopher;

He thought extremely deeply about everything, which included shareholder capitalism. He had the purest, single minded goal of simply generating profits and increasing wealth.

He was a capitalist through and through. To the extent that back then Top management meetings with Shigeta-san were called “Shareholder Report Meetings”

The meetings often (only?) discussed ROI and IRR (which in context of Japan, especially back then, I’d say is VERY rare).

Subordinates would have to present to the founder who will discuss and approach them not so much as a ‘superior’ but an investor. Approvals of new businesses ultimately then depended on whether it was a worthwhile investment. (In that respect, this feels quite similar to how Buffett operates Berkshire.) Shareholder Capitalism was truly his religion.

While the CEO is often thought to be someone who handles 100 different tasks, he was an essentialist who focused on the most important thing at that point in time. He fully committed to that one thing as the CEO and delegated everything else. That ‘one thing’ changed over time.

Some examples: his first goal was to create a high-functioning sales team. After that it was the relentless focus on getting the best terms with suppliers, so on and so forth. For each, after he reached a certain level, he would then hand off the responsibilities to his subordinates completely, moving onto the next thing he needs to fully focus on.

Hikari was not shy of using debt from early on - one of his ‘main goal’ at some point became securing the most financing possible, at which point he surrounded himself with bankers to get as much financing as possible. That’s the only thing he did, but relentlessly.

His idea was that anyone can do this as long as they fully focus on one thing rather than multiple things. This extended to how he managed people. To the division heads rather than making them pursue a multitude of KPIs, he’d reduce this to one or two and specifically focus on that, day in, day out. So throughout the year the reporting would be just that one KPI. His lessons as an essentialist still lives today. The podcast with the current CEO echoed those lesson from him which was to keep things simple - and to win where the competition is ‘easy’.

Somewhat related to this is that everything came down the bottom line. In a way this laser focus was ultimately to achieve the most important thing for Shigeta-san, which was a high ROI.

All he expected from you was business matters. Interestingly, Yamamoto-san does not know anything about the Founder’s personal life and nor does the founder about his. No small talk. All the conversations was on business, the KPI he was given, and the bottom line. This was despite the fact that he’s even been to his residence and had drinks together!

Finally, Shigeta-san was hyper-rational. There was an anecdote shared in this story of when he visited the office Son Masayoshi, the founder of SoftBank who was one of their main clients for ameeting. At that point in time, Hikari as a sales company drove the most sales for SoftBank, by far. Despite that when they arrived at the office, him and the vice-president were asked to enter the building through the back door. This was because Shigeta-san and Hikari was getting some negative publicity.

Hikari management was pissed. “Why on earth are we being treated like this after years of service, and generating so much sales for them?”

His response was surprising to many. “If I was Son-san I’d have done the same, because he needs to protect his own shareholders, clients, business partners”. In fact he was impressed that Son did that and was smiling about it.

If you had to remember one thing about Shigeta-san though, is unlike many older CEOs in Japan, he’s always respected the shareholders and thinks like an investor.

Now as an aside the founders son has way more press but not for any business reasons. On the news that he’s a surrogate father to 13 children! - and I don’t know how many grand children at this point!!

The new CEO

Over time Shigeta-san moved on to becoming Chairman and theres been CEO changes. The company is now led by Wada-san since 2019, a long time Hikari Tsushin man who’s climbed up the rank through intense competition. Unsurprisingly, shaped by his experience, he also believes in the importance of meritocracy. He made this pretty clear in Jake’s Quality Investing Podcast from the start. This is no surprise, Wada-san has also competed his way up to the top. He was the number one performer among new hires and got promoted only after 5 months.

One change which seems to have happened as a result of him taking over the reigns, is that it seems previously management has kept the investment business and the operating business quite separate from on another (other than the common thread that both required good IRR). In other words, the operational business did not really speak to interact with the companies in Hikari’s investment portfolio. As I understood it, since Wada-san became CEO they saw their investments in these companies as potential leads to which the operating business can sell to.

Nonetheless, the new CEO continues to keep up the spirit of competition and the Hikari Tsushin culture that Shigeta-san so cherished alive.

Culture

A key feature of Hikari’s business and what I think is their source of success is that on the business side, the organisation fosters a culture of frugality, customer focus and willingness to adapt. This all of course comes with an intense focus on return on Investment. The management understands the importance of their culture and deliberately looks to nurture this. Wada-san said himself, the business shouldn’t be dependent on the CEO. In other words he highlights the importance of keeping this culture alive. That focus should put many investors at ease when it comes to succession planning.

As you could’ve imagined based on the story of the founder, people who’s been to their original HQ in Ikebukuro say that it was in an old run down building (although they have since moved).

Hikari, perhaps more than any other Japanese company I know, has been the ultimate meritocracy, almost to a fault. Performance has been, and still is, everything. You were appropriately rewarded for that too. Someone asked in an interview why many applied to Hikari even during the time it’s notoriety was growing and people were dropping out like flies. The answer was that many joined to ‘win big’ by signing on that big contract that comes with potentially life-changing compensation.

Your background, who you are, where you’re from, your age, it simply does not matter. Now remember that Hikari has been doing this from early back when many organisations valued seniority more. If you performed, you were rewarded both monetarily and promoted up the ranks of the organisation. Although in a different shape, this spirit lives on today and is at the core of how Hikari operates, just as Wada-san emphasized.

In the past to be clear, it didn’t sound that difficult to get a job there either (back then, that is) because there were always vacancies. But it was also easy to be let go if you didn’t perform. (not sure how this works but it seems like many weren’t on full time contracts). As Yamamoto-san whom I mentioned earlier retold, it didn’t matter if you had a good year last year, if you don’t do well this year, you were out. However, Shigeta-san gave second, third, fourth chances too. That meant that even if you were ‘fired’ you could re-join and work your way up. There was no emotion involved, on the part of the founder, he would talk to you as if you never left in the first place.

Their culture of course, has also evolved as times changed; it wasn’t always as clean as it looks today, but they seem to have come a long way. The company has since made their compliance much stricter and started implementing measures to improve employee satisfaction and in order to adapt to the new labour market needs. Looking at employee reviews it’s pretty remarkable how many people credit their experience at Hikari for personal growth - because you were given responsibility early.

Now early on, the intense culture also hurt Hikari as you will see later.

Some legendary stories of Hikari emerged too. So much so that they even invented a word that gets used in the company. From how I understood it, Hikari employees would use the word “Zosu” (ゾス) as a form of greeting. This is not a real word but multifunctional word which can be used in place of anything like “Good morning”, “Understood”, “thank you” etc etc. Pretty much any kind of greeting, you do away with Zosu!

Hikari Tsushin’s Dark Past

And it might sound pretty hilarious and culty but it gets pretty dark. As I said, their well sounding culture wasn’t all too clean in the past. Hikari was infamous in the past (15+ years ago) for questionable labour practices. So it was formerly known for being a black kigyo (ブラック企業) - a designation a company in Japan gets for being exploitative. There’s an extensive list of such companies and new graduates and job hunters alike, will certainly take note if your company ends up on this list. Going through interviews of past employees who worked in that period, I’ve collected a few stories.

I’d like to add here though that, theres been quite a few interviews with former employees and pretty out in the open for this - but theres naturally a bias bc generally they’d only be getting interviewed if they had some kind of strong opinion. Theres also the sample size issue because it’s really more a summary based on a handful of people. (Granted that opinions have been consistent). Also remember that even just 20+ years ago, what was seen ‘harsh’ today was more normal back then… I’d bet some of the other well-known companies also had harsh conditions, but are just less talked about in this way. (In fact theres plenty of examples of this) We even describe the harsh/tough working environment of back in the day as ‘Showa’ style, referring more or less to “how things worked” in the showa era.

Employee Interviews:

There was one fascinating interview that shared a few tidbits about the company. It was his first job out of university. He was presumably there until around 2016. So it’s not even too long ago.

[Here is the link for the gentleman being interviewed in Japanese, if you look at the comments this may give an idea of how the company is perceived by the average Japanese] Part1, Part2 and Part3

Theres so many others like here. Alot of the stories were pretty consistent with another.

Apparently the manager told him “you can either choose getting a appointment with a lead, or death” (lmao wut) →[To be clear this was not literally I’d think! but really showed the intensity of as if they were going to war]

As a sales person you’re always cold calling, no conversations in between. You basically need the phone physically attached to your face’ the whole time. If you don’t your manager will be breathing down your neck.

By the time he joined. the company was already starting to crack down on compliance so at least ‘officially’ your day ended at 9pm.

You’d sometimes hear a loud bang! in the office. That was one of the managers kicking the desk to intimidate his subordinates. Almost all desks had some kind of dent in them from kicking/punching (lmao)

Plastic bottles filled with liquids were flying across the office aimed at people.

Whilst this wasn’t completely unique for a black kigyos, your manager had to be aware of your whereabouts constantly. You need to call to ‘check in’ with your boss before every sales appointment. He’d also call during your sales meeting in front of a potential customer, screaming. So loud that they might even hear it. You also had to call after your sales meeting regardless of if they managed to close a customer. You can imagine what happens if you didn’t. (Answer: the manager will scream at you and make you go back inside to talk to the lead again, even if he’s already said no pretty clearly)

As a new hire, your inauguration basically sounded like hazing…their offsite for new hires was infamous and got mentions in several interviews I watched.

In terms of employee attrition another former employee remarked out of 300 new hires maybe 10 remained in 3 years time at best.

However not all was bad. They were extremely good at sales as a result. For example, when Hikari acquired a company which was a number 2 or 3 player in a market they would then use their sales prowess to get to the no.1 position. One project he worked on, reached the top market share in 6 months.

Besides, why did people continue to join Hikari? because if you performed, the incentives were really that good. Those that joined in the early days weren’t necessarily elites, but they were looking for chances in life and Hikari offered that in spades.

He ends with a fair remark that Hikari seems to have improved a lot over the years and many of the ‘traditions’ mentioned above no longer exist - especially as a public company which subjects you to more scrutiny and stricter compliance + in the age of social media, it seems that it’s hard to work that way. In more recent years, private companies run by ex-Hikari seems to inherit the ‘old’ culture more.

Another story I’ve come across a few time is about their company motto. Employees in the early days had to recite this out loud. No, not just at the office in the morning to get pumped but even when you had to call in to HQ from a public phone booth (mobiles didn’t exist back then). This apparently extended to your orientation offsite that happens when you first join the company. As the legend goes, you’ve had to recited this ALL day, in addition to other strenuous activities. This offsite seems to have had a military feel to it…

There is an interesting piece about this all from the Founder of UUUM a previously listed company that got acquired just this February.

HIKARI TSUSHIN company motto (Translated)

We should always act with romance and aesthetics.

We should always act with humility and honesty.

We should always act in harmony with the whole.

We should always act with true energy and purity of purpose.

We should always act with the belief that beyond the impossible lies the possible and beyond giving up lies success.

Director Interview:

There was this other interview that I found fun to watch from Yamamoto-san (and also made me think, thank f*** I wasn’t there) He highlighted a few company ‘customs’ back in the day, which really fleshes out some details about the ‘cult’ of Hikari Tsushin so scary that it’s almost comical. He highlighted a handful out of 100+ expected ‘rules’ back when he was there. Once again, you can’t help but feel there was a military feel to it back in the day. Alot of these interviews recalled their day to day as if they were ‘going to war’.

“Every Sub manager had 4 or more people working for them. They’d be assigned positions like ‘right hand man’(in Japanese strictly translated, more like Right arm), ‘left arm’, right leg, left leg and others. Your rank changed every day based on your performance from the 1st of each month. Your seniority, gender, background did not matter. Being the right hand was being the ‘god’ and everyone else had to speak to higher ranks in Keigo (respectful, Honorific Japanese).

Based on your rank, even your desks looked different, ‘Right hand’ had nice office chairs, with arm rests. ‘Left arm’ didn’t. Now these were the two ‘highest’ positions. The lower your rank went, well… you can imagine!

But it doesn’t end there - the sub managers also get ranked among other ‘sub managers’ and this system continues up the hierarchy. The general rule being that you get treated worse the lower you ranked among your peers. This fostered competition among all levels of the organisation. Team, department, division etc, etc.

All that mattered were your numbers. Truly the old school “Always Be Closing” mentality meant everyone competed. You weren’t really addressed by name, but by your designated rank and team. So much so that, you weren’t even allowed to talk or make eye contact to those in other departments or teams. They saw no point because in reality, they were your competition. You beat them today so they don’t talk trash to you tomorrow. This went on and on and on…

You were also banned from complaining to yourself, like “I’m cold” or “Im hungry”.

You can ultimately summarise this to the fact that, the lower rank you are, the less you deserved, in essence this goes back to the idea which was that this company took meritocracy at the utmost extreme. If you didn’t deliver you don’t ‘deserve’ to use the bathroom, or eat, or drink.

Here’s another one: There was no ‘slow’ walking to the train station, you speed walk or run and nothing below that. That would be a waste of time.

Now having said that, the aggressive sales style in the past has led to some counterproductive outcomes. This culture at one point became too hostile, and came back to bite them in the a**. I mentioned earlier that one of Hikari’s divisions were booking fictitious sales of mobile phone contracts. The root cause (in my understanding at least) has been that because of the intense fear of having to meet KPIs that are almost impossible to achieve - this led to employees booking such fake sales to please their managers, to avoid being screamed at and belittled. No, these employees shouldn’t have done that and they need to take responsibility for that - but it was also a moment to realise this culture of fear can have unintended consequences. Despite Hikari’s intentions being good.

Perhaps as a combination of all the “hikari stories’’ of the past and the fraud scandal, I feel there may still be some stigma around the company among Japanese people. Which is understandable. Now that I come to think of it, maybe their JV with Constellation Software didn’t go as well as they intended as sellers may have feared selling to a company with a dark history (but to be fair, Constellation is not a widely recognised entity in Japan so sellers probably also thought “who the hell are you!”). These are just merely personal theories of mine of course!

Nonetheless, what’s undeniable (I think) is that because of the hardships faced by working at Hikari- this also created some of the most resilient business people in Japan. There was another interview of a different former employee, and despite the hardships, he credits Hikari for making him mentally tougher when starting his own business. Yamamoto-san mentioned managers that left Hikari and who’d consequently start their own business would continue to work with Hikari - and that you wouldn’t do that if it was a truly an evil company. I think that’s a good point. Other stories included how one would move on to another reputable companies and felt that the sales reps were ‘lukewarm’ compared to Hikari, it wasn’t that they were bad- just that Hikari had that much more intensity to it. Many of these guys, despite the difficult time there, were battle hardened.

From a customer’s perspective - imagine, if you have a company that’s so dedicated to selling your product, that’s pretty darn reassuring partner to have. Remember, they reigned as Softbank’s top sales partner at a point in time and also have demonstrated time and time again, their ability to gain market share whatever category they played.

Overall

So this has been a little bit about the operating side of the business. I’ve tried to pack the most interesting things in here. Regrettably it feels less structured but its just because theres so many interesting stories to this business.

In reading this, I hope you got to understand a little bit more of the “japanese perspective” I wanted to have a more nuanced take and balance it out because I think it’s not entirely fair to circle out Hikari for being a Black Kigyo. The reality is that there are plenty of companies that had pretty harsh environments. Lets all remember that this was post WWII Showa-era where rules around employee protection were less defined. A potentially interesting way to frame this story is also that Hikari, despite these notorious practices somehow managed to flourish over the decades. Through many trials and tribulations, they’ve learnt to be anti-fragile. Despite the countless leavers, somehow they’ve still managed to get new people. This system may not have been for all, it’s ruthless and almost mechanical, but its worked as a business model remarkably well.

It’s also not so much of a surprise that the interviews of those who were higher ranked in the organisation tended to remember Hikari in a better light. Winners stayed on - so I think those that were higher ranked were rewarded in Hikari’s environment of absolute meritocracy - there was less reason to scorn.

Today the business seems to continue to improve, that’s another component that many of these interviews pointed at, which was that by the time they left, things were already getting better. You might wonder With so much of this ingrained in the DNA of Hikari , will things truly change? But things really seem to have improved when glossing over some of the employee reviews on Openwork (The glassdoor of Japan). This has been helpful to get a much more nuanced view on the company versus the general perception by many in Japan. It kinda makes sense, if there is a profit incentive (and to increase shareholder value) to improve employee satisfaction, I’d count on Hikari to do this relentlessly. That’s what makes them so damn good.

Anyway, let’s wrap it up for today. I hope you’ve now been able to seen potential reasons why this company has been discounted by the market for so long through the Japanese Perspective.

In part 2 I’ll be writing abit more about Hikari Tsushin the ‘investor’ I’ll try to cover stuff like Investment Philosophy/Capital Allocation, Valuation, How investees perceive Hikari and the potential risks to the business.

Disclaimer: The content on this website is for informational and educational purposes only and is not created to meet your personal financial situation. Nothing should be considered as investment advice or as a guarantee of profit. You are advised to consult with your financial advisors to discuss your investment options and whether it would be a suitable investment for your personal needs. The information used in this publication is from sources that are believed to be reliable but the accuracy cannot be guaranteed. It may include some errors, please make sure to do your due diligence. The opinions expressed are those of the author and the author only. These opinions are subject to change without prior notice.

Does the stigma have something to do with the news of employee overwork leading to death? And do you know when did the company start to focus on pure investment as a business?

Looking forward to part II