A quick note on a Japanese Appfolio

A sticky Real Estate SaaS company that could trade at 10.5x Normalised P/E next year...

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclosure: The author currently owns shares in the company as of 17 April 2024. The security could be sold at any point in time without prior notice.

I’m trying something different as I tinker with this platform. This will be a short note and an idea on a trade, which could turn out to be something more interesting as time goes on…

TLDR: Real Estate SaaS Company down on a temporary issue. Should be trading at 10.5x P/E on a normalized basis once the results roll over.

There’s a company that bombed on earnings recently and went down 30% at the bottom (such is the world of micro-cap land in Japan). Up a bit since but nowhere near where it was before. I think the earnings reaction was too harsh for what should be a positive for the longer term - and therein lies the opportunity. The company is Property Data Bank $4389

Market Cap: 7 billion Yen

P/E: 27x*

ROCE: 18.5%

5-year Revenue CAGR: 18%

5-year EBIT CAGR: 28%

The business is a Real Estate Asset Management ERP used to manage corporate properties throughout its life cycle. I am told that Appfolio APPF 0.00%↑ is a similar company in the US.

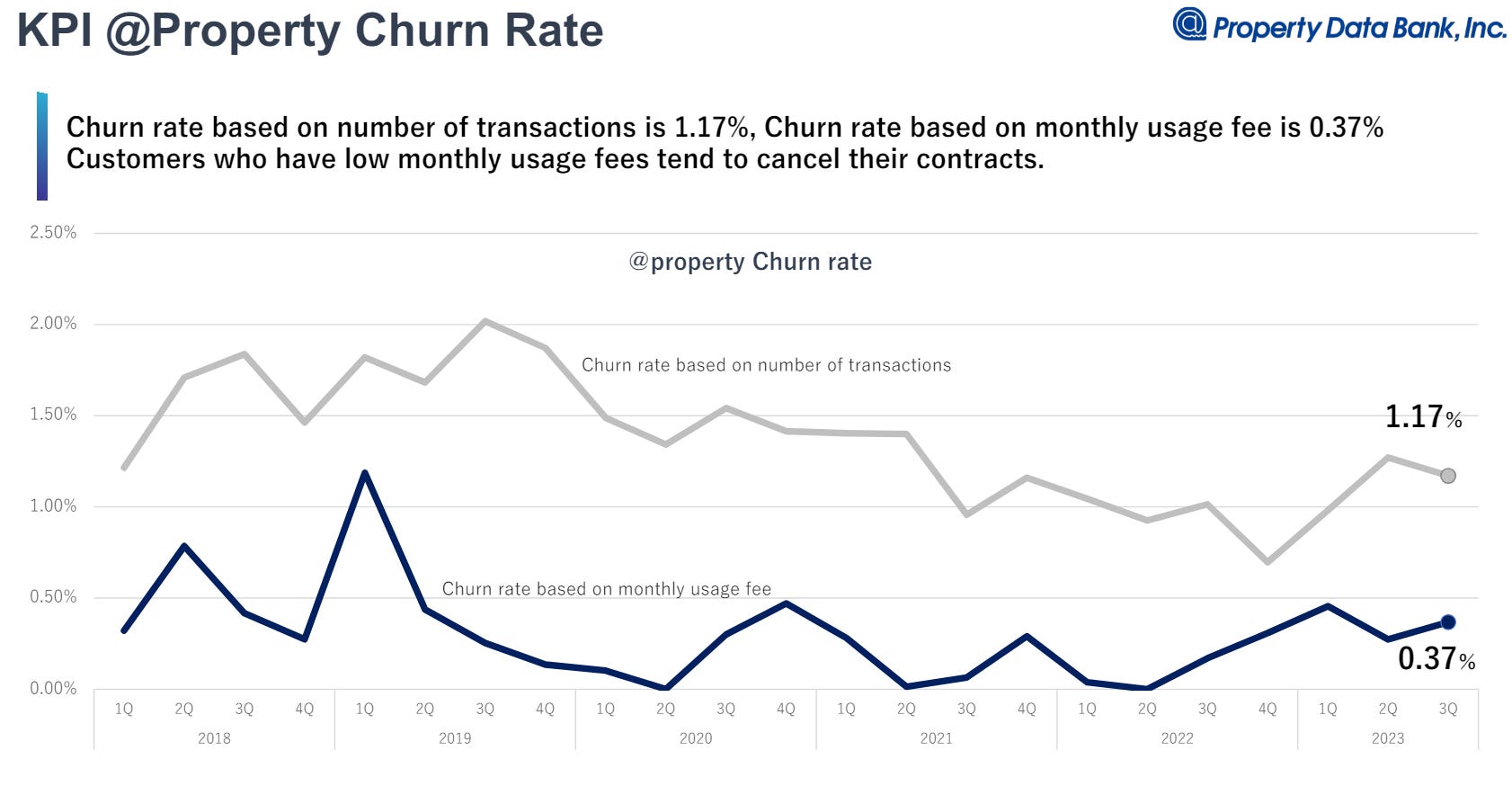

Property Data Bank shares similar traits with APPF as far as I can tell and I like the business (albeit not as good). They are owner-operated (Founder/Chairman owns 9%), have a very sticky platform that’s almost impossible to churn from (Monthly revenue churn of 0.27%), and customers become increasingly reliant on them as they involve more and more of the relevant stakeholders to use the platform. (read: add-on services). This has also led them to amass a huge repository of property-related data.

It’s also got a formidable position in the property market with >50% of J-REITS as customers and serves well-known corporations (like Shiseido) to help manage their corporate assets. I should add, that 70% of the top 15 railroad networks also are customers.

It has a mix of implementation, which are non-recurring, and subscription revenues. The split is about 50/50. This is important to remember for the next bit. Like a typical software company though, they’re profitable and have been since its 3rd year after it was founded. Usually in the >20% for operating margins these days.