A quick note on a Japanese Appfolio

A quick note on a Japanese Appfolio

A sticky Real Estate SaaS company that could trade at 10.5x Normalised P/E next year...

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclosure: The author currently owns shares in the company as of 17 April 2024. The security could be sold at any point in time without prior notice.

I’m trying something different as I tinker with this platform. This will be a short note and an idea on a trade, which could turn out to be something more interesting as time goes on…

TLDR: Real Estate SaaS Company down on a temporary issue. Should be trading at 10.5x P/E on a normalized basis once the results roll over.

There’s a company that bombed on earnings recently and went down 30% at the bottom (such is the world of micro-cap land in Japan). Up a bit since but nowhere near where it was before. I think the earnings reaction was too harsh for what should be a positive for the longer term - and therein lies the opportunity. The company is Property Data Bank $4389

Market Cap: 7 billion Yen

P/E: 27x*

ROCE: 18.5%

5-year Revenue CAGR: 18%

5-year EBIT CAGR: 28%

The business is a Real Estate Asset Management ERP used to manage corporate properties throughout its life cycle. I am told that Appfolio APPF 0.00%↑ is a similar company in the US.

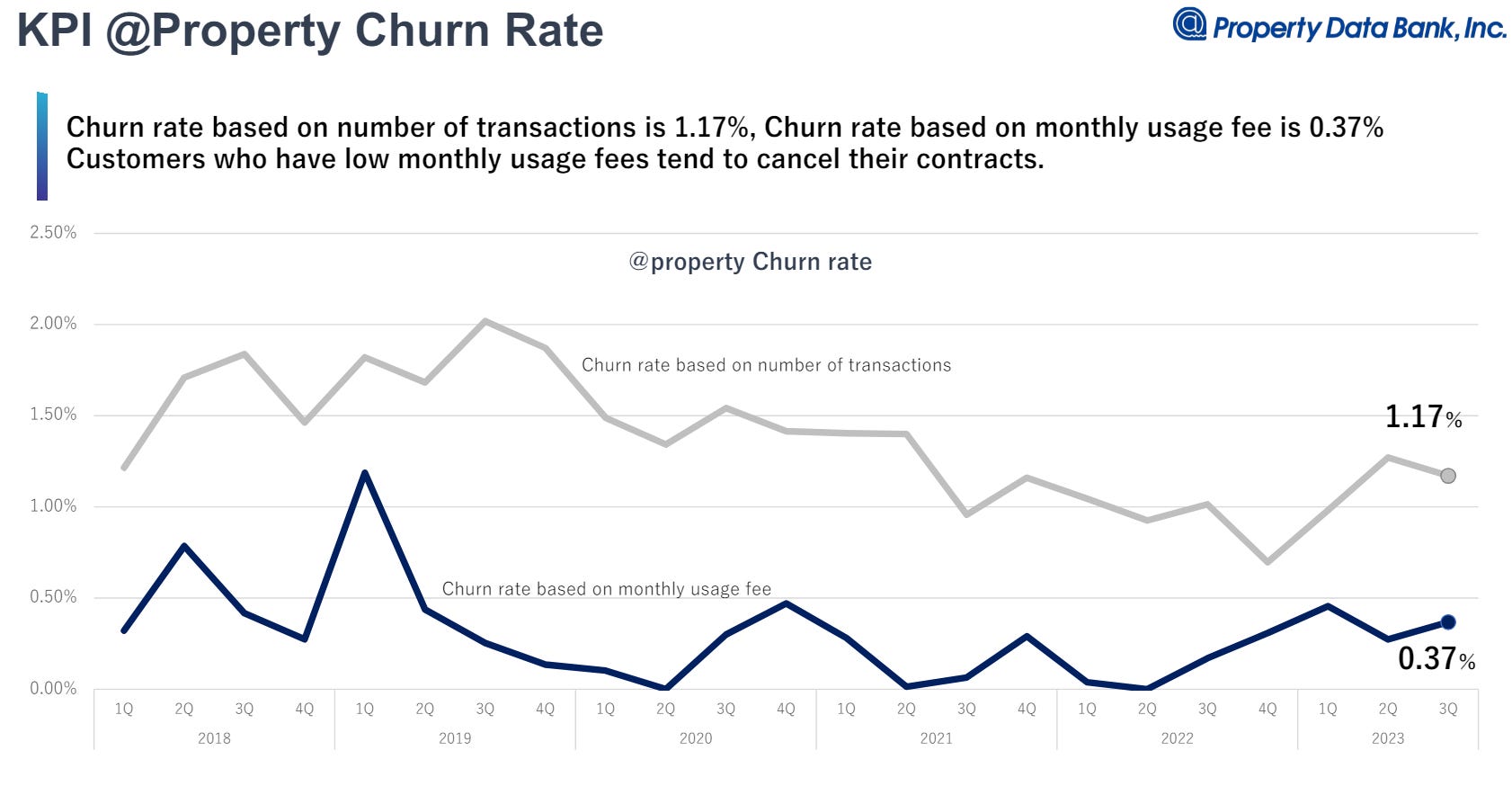

Property Data Bank shares similar traits with APPF as far as I can tell and I like the business (albeit not as good). They are owner-operated (Founder/Chairman owns 9%), have a very sticky platform that’s almost impossible to churn from (Monthly revenue churn of 0.27%), and customers become increasingly reliant on them as they involve more and more of the relevant stakeholders to use the platform. (read: add-on services). This has also led them to amass a huge repository of property-related data.

It’s also got a formidable position in the property market with >50% of J-REITS as customers and serves well-known corporations (like Shiseido) to help manage their corporate assets. I should add, that 70% of the top 15 railroad networks also are customers.

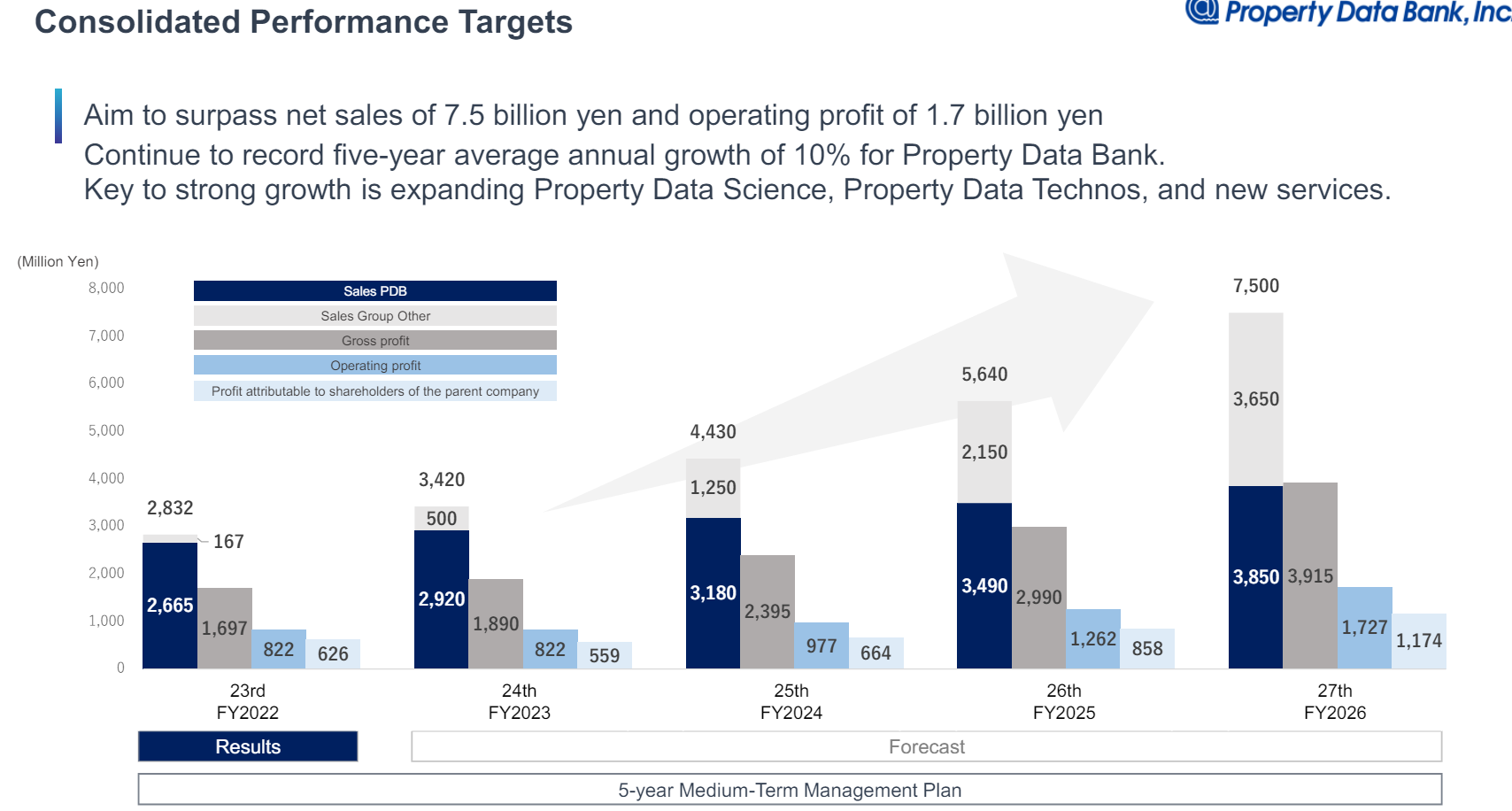

It has a mix of implementation, which are non-recurring, and subscription revenues. The split is about 50/50. This is important to remember for the next bit. Like a typical software company though, they’re profitable and have been since its 3rd year after it was founded. Usually in the >20% for operating margins these days.

What happened:

They revised their sales guidance down for the year by -26% and earnings by a whopping -56%. Yuck.

Now, the reason earnings went down so much though was some of the clients they’re working with are putting on additional orders for customization. This made it more complex and delayed the revenue booking to next year and since it is related to implementation revenues (that’s the non-recurring part) it looks terrible. This portion can be volatile depending on the year and looks even worse due to very tough comps from last year.

The business costs are mainly fixed (people/devs) so there's some negative operating leverage when revenue declines. At the same time, management is going ahead with investing for growth to achieve its mid-term plan (mainly hiring) squeezing the margin even more this year.

It doesn’t help that the new President’s expectation management has been terrible, so I get why the market is frustrated. The president presented a mid-term plan targeting a 30% revenue CAGR from 2022. Far higher than in the past but dependent on new adjacent business with little to prove thus far. Fumbling so soon is not a good look.

Looking through this mess, however, the pipeline of customers and new customization orders for its core business remains healthy. (in the neighborhood of 2-3 billion yen), so that’s likely to return. Its subscription part is business as usual - increasing steadily albeit slowly. In fact, implementation revenues translate to subscription revenues with a 2-year delay, given that 2023 was a good year for implementation revenues, we could even see strong growth in subscription revs for 2025. So the core business hasn’t fundamentally changed except that customer orders are getting larger and demand remains strong.

So let’s say revenues go back to par versus previous levels next year, it’s feasible because, in theory, the implementations are larger (so actually, it should do better if anything…). Also assuming operating margins come in line with its medium-term target of 22%, that’s a 12-month forward P/E multiple of 10.5x excluding cash - For a growing, profitable software company, and minus the bad year, I think there’s quite some room to grow left.

I also believe they are under-earning, since they amortize IT Capex over 3 years, which is quite aggressive for a highly recurring biz IMO.

If the market decided this business sucked because they had to delay revenue recognition by a year, I’m interested to see what’ll happen if the company forecasts strong growth from an easier comparison base for next year.

On a longer horizon, things can also be interesting.

Their new initiatives so far don’t have much to show, so it’s not wise to attribute a high probability of it materializing just yet but at the valuation today, we’re essentially getting upside from its core business that’s been doing well (with one big hiccup of course - but a 10.4% revenue and 17% EBIT CAGR since listing nonetheless [13.4% revenue CAGR and 31.5% EBIT CAGR if you exclude this year] ) and whatever new products they’re working on to accelerate their revenue growth to a 30% CAGR comes for free.

The prospects of such an acceleration are still questionable, but it is not completely baseless either. They are working on BPO and AI-driven solutions apparently with some good interest from retail chains for the latter. Some of the solutions they’re developing have a high chance of achieving product market fit since they get developed through discussions with existing clients (and consequently, can up-sell easily). They could overspend and run the company to the ground, but they’re conscious of ROI and plan on keeping EBIT margins above 20% which is easily achievable through their core business. Their ROI focus is why they’ve done a good job staying profitable since they’ve listed. This leads me to believe going back to at least 20% is likely, and in the longer term won’t burn too much cash. I also learned that its BPO business is already profitable. Historically, the management has sandbagged expectations repeatedly, and they seem to be projecting margins quite conservatively again.

Big picture, $4389 is well established and has been running profitably from almost the beginning (they have to, large customers won’t use you otherwise due to continuity risk). So with the core business already undervalued and its new pillars coming for free this looks like a pretty asymmetric opportunity. With the founder still on the board, I don’t think the business will turn to dust. The worst case in my view is that he’ll get rid of the President if he mismanages. Guess we’ll see how the market reacts for Q4, when they provide guidance, and/or when they report results in Q1!

As there’s so many interesting ideas, I’m thinking of sharing more ideas in short form like this in addition to some deep dives. Let me know your thoughts.

Tata for now!

Disclaimer: The content on this website is for informational and educational purposes only. Nothing should be considered as investment advice or as a guarantee of profit. Please make sure to do your due diligence. The opinions expressed are those of the author and are subject to change without notice.

Disclosure: The author currently owns shares in the company as of 17 April 2024. The security could be sold at any point in time without prior notice.

Love this one

Another great write-up